Inflation Bites into Fast-Food Profits

Following a period of relative stability in 2024, entering 2025 inflationary pressures in the UK’s economy have resurfaced according to a survey from market intelligence company Meaningful Vision.

Year-on-year price growth, as measured by Meaningful Vision’s Foodservice Inflation metric, and the Office for National Statistics’ Food & Beverage Inflation numbers, showed foodservice inflation experienced a cooling-off from highs of 13% in late 2023, settling to a more manageable 5% in 2024. This stabilisation likely offered much needed respite from rising prices, for both operators and consumers.

However, January 2025 marked a turning point as the foodservice inflation resumed its climb reaching 6%, the highest point since early 2024. This return to an ascending trajectory signifies a renewed wave of inflationary pressure hitting the sector.

By comparison, the ONS Food & Beverage Inflation rate showed a less dramatic increase, moving from 2% at the end of 2024 to 3% in January 2025, indicating the resurgence is currently more pronounced within foodservice.

Having tracked over 60,000 of the UK’s top food outlets – including quick service restaurants, casual dining establishments, bakeries, coffee shops and pubs – key insights emerging between 1st January – 28th February 2025 include:

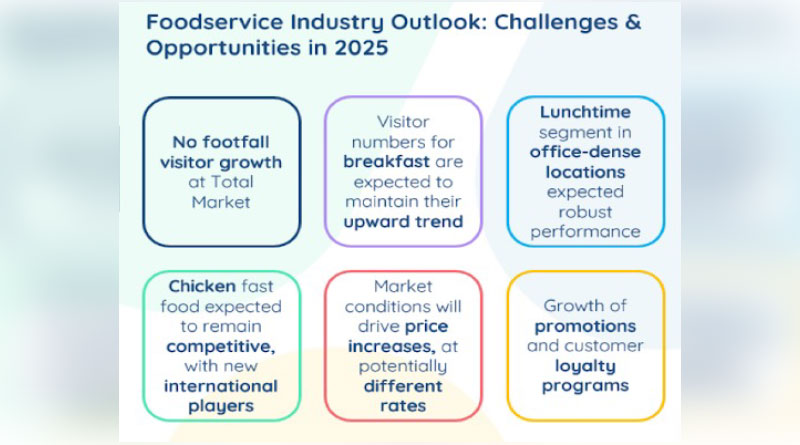

- Store growth: The growth rate of new store openings across the market was up 1.0% in Jan-Feb 2025 vs. 2024, while fast food stores were up 2.1%. Quick Service (QS) Bakery & Sandwich and QS Ethnic segments remained on their growth trajectory from 2024, while chicken shops saw an uptick in performance following a surge in openings from new international players. However, overall figures were lower than Jan-Feb 2024, suggesting a slight deceleration in expansion.

- Consumer traffic: Across Jan-Feb 25, market traffic across the industry declined by 2% compared to 2024. Restaurants experienced the largest drop, down nearly 8% overall ( -7.7%), while pubs were down by 6.2%, having previously increased by 2.7% from 2024 vs 2023. While footfall continued its negative momentum into early 2025, February’s decline was partly driven by calendar variance, with one fewer trading day than last year.

- Time interval footfall: Morning visits in Jan-Feb 25 vs 24 demonstrated some drop compared to 2024 vs 2023 data, which showed an increase of 13.8%. On the contrary, data shows the previously declining 3-6 PM hours and evening visitor numbers begin to recover; the daytime slot of 3-6pm showed an increase, up 1.7% for Jan-Feb 25 vs 24, while evening visitors also rose slightly, up 1.1%. This could be attributed to a gradual return to post-work socialising and snacking on the way back home. Bakeries and coffee shops were the main contributors to the increase in visits during the period between lunch and dinner.

- Regional data: Compared to the UK as a whole, London performed better across Jan-Feb 25 vs 24, up 0.9% (compared to the UK at -2.8%), a trend we also saw in 2024 vs 2023, with London up 3.9% (compared to the UK at -0.8%).

- Prices: The rate of price increases during Jan-Feb 2025 reached 6% in restaurants and 3% in retail, showing some increase compared to December 2024.

- Promotions: While 2024 saw restaurants increase the number of promotional offers by 25%, so far in 2025 this increase has reached 15%. Offering special prices was a top tactic among price promotions in restaurants, up from 70% in 2023 to 71% in 2024. Conversely, Percentage Discount was top within delivery, rising from 34% to 49% in 2024; trends also seen in 2025 in terms of promotion types.

Maria Vanifatova, CEO of Meaningful Vision, comments:

“As predicted, the start of 2025 has been tough, with a marked slowdown in those eating out as consumers adjust spending habits in response to economic uncertainty. We’ve also seen tough market conditions drive price increases. Though this was recorded at 6% Jan-Feb this year, with government tax changes set to push inflation up to 7-8% from April, price sensitivity will likely continue affecting footfall negatively.”

“Despite these challenges, we are seeing some signs of positivity, with fast food stores expanding, and daytime and evening footfall experiencing some signs of recovery. We’re also expecting healthier-focused chains to grow in popularity and rising office attendance support the demand for convenient morning and lunch essentials like coffee and sandwiches – the AWA reported a 20% increase in office occupancy in 2024, with large firms expected to return to five-day workweeks within three years.”

“It’s positive to see, even amid economic pressures, chains are already taking advantage of these opportunities, with Limited-Time Offers (LTOs) and meal deals proving effective, and healthier options capturing new consumers. Maintaining resilience in 2025 will be about keeping a keen eye on these consumer trends, tracking what works and what doesn’t, and adjusting promotions and offerings accordingly.”